Australia’s $24B Digital Asset Opportunity Hinges on Regulatory Clarity

Linda Titianitus2026-04-24

Linda Titianitus2026-04-24

Australia could unlock A$24B yearly from tokenized finance, boosting efficiency and access. But without clear regulation, uncertainty may stall adoption and push capital elsewhere.

Australia is on the verge of one of the biggest financial upgrades in recent times it just all hinges on regulation. If Australia gets it right, the country could draw A$24 billion ($17 billion a year) worth of benefits from digital assets and tokenized finance something a joint report from the Digital Finance Cooperative Research Centre (DFCRC) and the Digital Economy Council of Australia believes is well within reach. But only if regulators are prepared to guide the development.

The report‘s message is simple. The technology is there, the capital attractive, yet the regulatory uncertainty is preventing everything.

Tokenization as a Structural Shift in Financial Markets

The premise behind this opportunity is tokenization, or the digital representation of real world assets on a blockchain platform. Through digitization, assets could be transacted at near real time, without requiring time-consuming, multi-intermediary, settlement processes.

In reality tokenization has the potential to revolutionise the way markets work and enhance current market liquidity. It could minimize frictions across the different asset classes such as FX, stocks, govies and funds, where the speed at which an asset moves or its inherent liquidity has been limited.

The DFCRC report indicates that this change might even enable potential efficiency gains, especially in fields where posting delays and other operational complexities currently hinder performance.

Faster Settlement and More Efficient Markets

One and possibly the most obvious can be seen through the settlement speed. Conventional finance procedures often involves several layers of verification and clearance, which could be days in some cases.

Settlement can be instant using tokenized systems thanks to the blockchain infrastructure. This greatly reduces counterparty risk, while releasing previously blocked up capital throughout settlement cycles.

Another big aspect is automation. Smart contract systems will be able to perform financial transactions automatically, without requiring human administration, thus saving a considerable amount of administrative work for organisations.

Tokenized Money and Cross Border Payments

The paper also emphasises on the disruptive potential of tokenised money in international payments of the future, comprising both central bank digital currency and privately floated stable-coins.

The Market for stable coins and CBDCs could also greatly lower the cost and time of cross border transfers. By avoiding the traditional correspondent banking networks which are often slow, costly and full of middlemen.

In comparison, systems of tokenised money may facilitate close to real time settlement transactions across borders, thus reducing the costs involved for businesses and financial institutions or the general public involved in international trade.

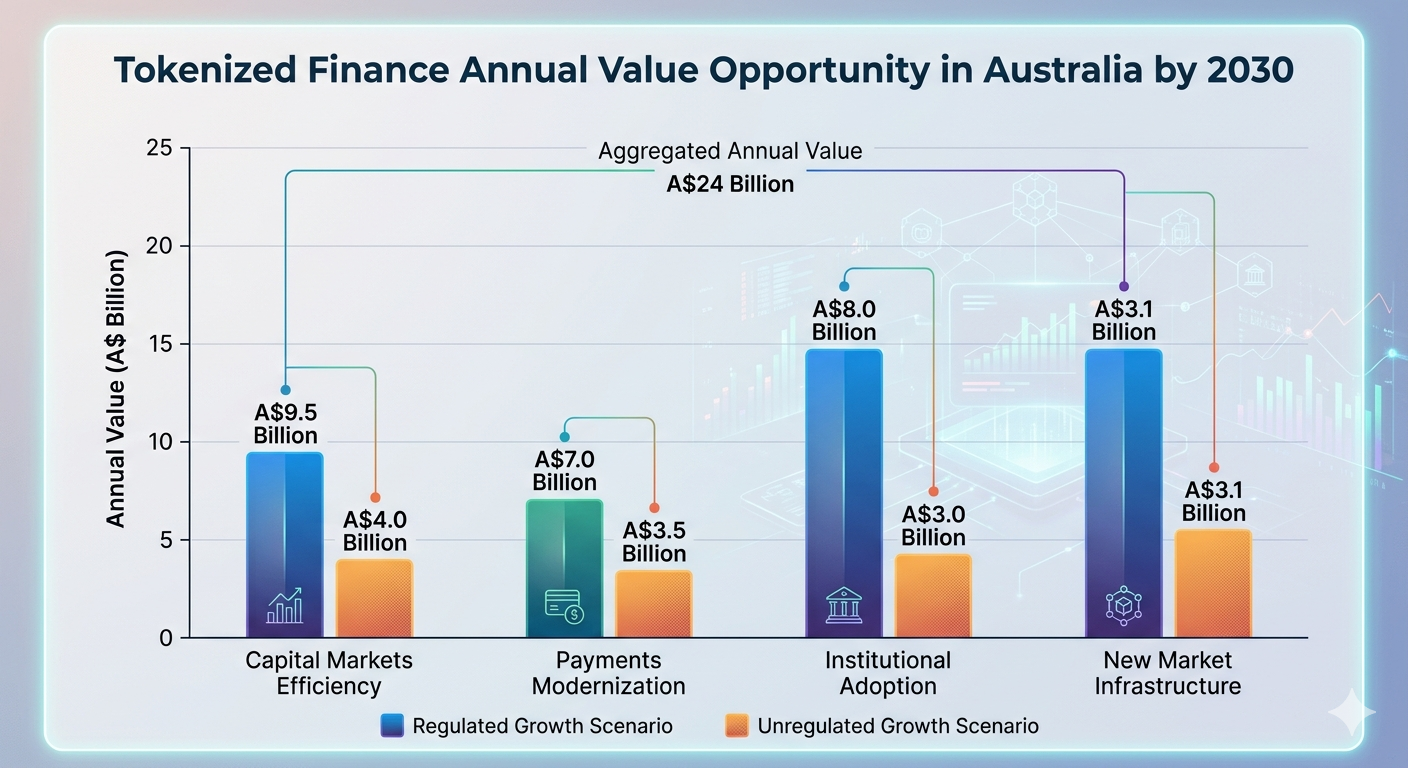

The $24 Billion Opportunity Breakdown

The a24 billion opportunity identified by the DFCRC analysis is generated from sources within the financial system such as increased market efficiency, expanded investor participation, and reduced infrastructural costs.

The report stress how value creation is not sector specific. All the different sector such as capital markets, payments systems, asset management and institutional finance create value to their customers.

But this value can only be achieved through the development of technology and regulation together.

Regulation as the Deciding Factor

Inevitably, despite being technologically prepared, the biggest obstacle for adoption is regulatory uncertainty. Financial institutions are unwilling to use their capital on such a massive scale before having better understanding of this space.

Key unresolved issues include:

Licensing requirements for providers of digital asset services.

Custody criteria for tokenized assets

Compliance frameworks for institutional participation

Legal definitions for digital securities and tokenized instruments

In absence of proper guidance, banks and asset managers are unlikely to adopt tokenization into their fundamental businesses.

The DFCRC report emphasizes that regulatory certainty is not just helpful but absolutely necessary to enable broad institutional engagement.

Institutional Investment Depends on Certainty

Tokenized assets could save a big financial institution money through improved efficiency but navigating the regulatory environment for such products might turn out to be too costly.

This creates a paradox where:

Technology completed and ready to be used

Market demand is increasing

Infrastructure is more mature, more complete, and easily available Uuenen (2008).

Uncertainty persists, however,...and the capital remains hesitant.

The report maintains that if this mismatch is not addressed then Australia risks being left behind other such financial centres who are moving forward on digital assets.

Australia’s Position in the Asia Pacific Digital Economy

Australia is considered to be among the most mature financial system in the Asia Pacific region. Its banking infrastructure is strong, and has a mature capital market and high technological levels.

But on the quickly growing discipline of tokenized finance, it is competing increasingly with more agile players, jurisdictions that are advancing more quickly on regulation and digital-assets.

Nations that make the rules early stand to gain in FDI, human and physical capital.

The A$24B Opportunity: A projection of Australia’s tokenized finance growth, showing how regulated frameworks maximize value across capital markets, payments, and institutional adoption.

How Tokenization Could Reshape Investment Access

Greater accessibility is arguably the most notable innovation brought about by tokenized finance. As assets are divided into smaller digital chunks, more investors will have the ability to participate in markets that were formerly available only to wealthy institutions or investors.

This could include fractional ownership of:

Government bonds

Stocks for portfolios: Equity

130 direct investment stocks screened by IBM with data sort ascendant in bandorad by industry.

To fundreal estate:

Foreign exchange instruments

Among foreign exchange instruments; Forward foreign exchange contracts are mostly used as derivatives. These are deals where price is agreed at the time of agreement but delivery of the value is made at some specific time in the future, these dates can range from one month to one year ( Taylor 2004, p 19). These can be put into two types; buying an end date and selling an end date.

Such changes might democratize access to financial markets, while improving their overall liquidity.

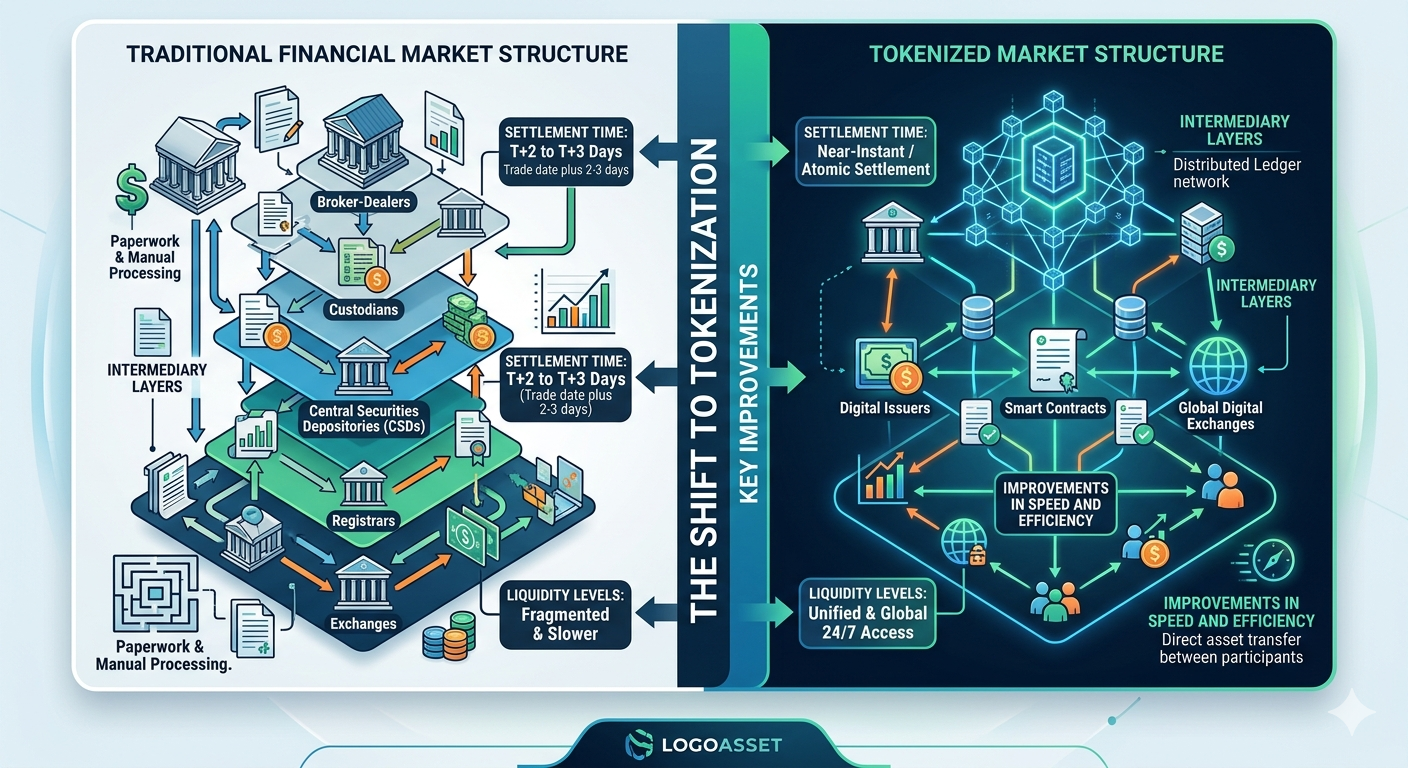

Evolution of Market Structure

A comparison of Traditional vs. Tokenized systems, showcasing how moving from multi-day manual processing to atomic settlement and smart contracts removes friction, increases 24/7 liquidity, and drastically reduces intermediary costs.

Conclusion

The A$24 billion opportunity in digital finance for Australia is not merely an upgrade in technology; it is a structural shift in how financial markets could work.

However, the report is clear that this opportunity is by no means assured. The kernel of the report is that the key determining factor for successfully reaping billions in value or losing out will be the speed and timeliness with which regulators put in place a firm regulatory framework.

Now, as tokenisation and the development of digital assets and stable coin based ecosystem surges across the world, Australia is at a ‘turning point’. The final result of Australia‘s policy and approach in the short-term will either see it emerge as a trail-blazer or a ‘tragic follower’.