Nexo’s Return to the US: From Regulatory Exit to Compliance-First Reentry

Natalia Ivanov2026-04-23

Natalia Ivanov2026-04-23

After a $45M settlement, Nexo re-enters the US, shifting from a direct yield provider to an infrastructure layer. By partnering with Bakkt, it uses regulated intermediaries to ensure compliance.

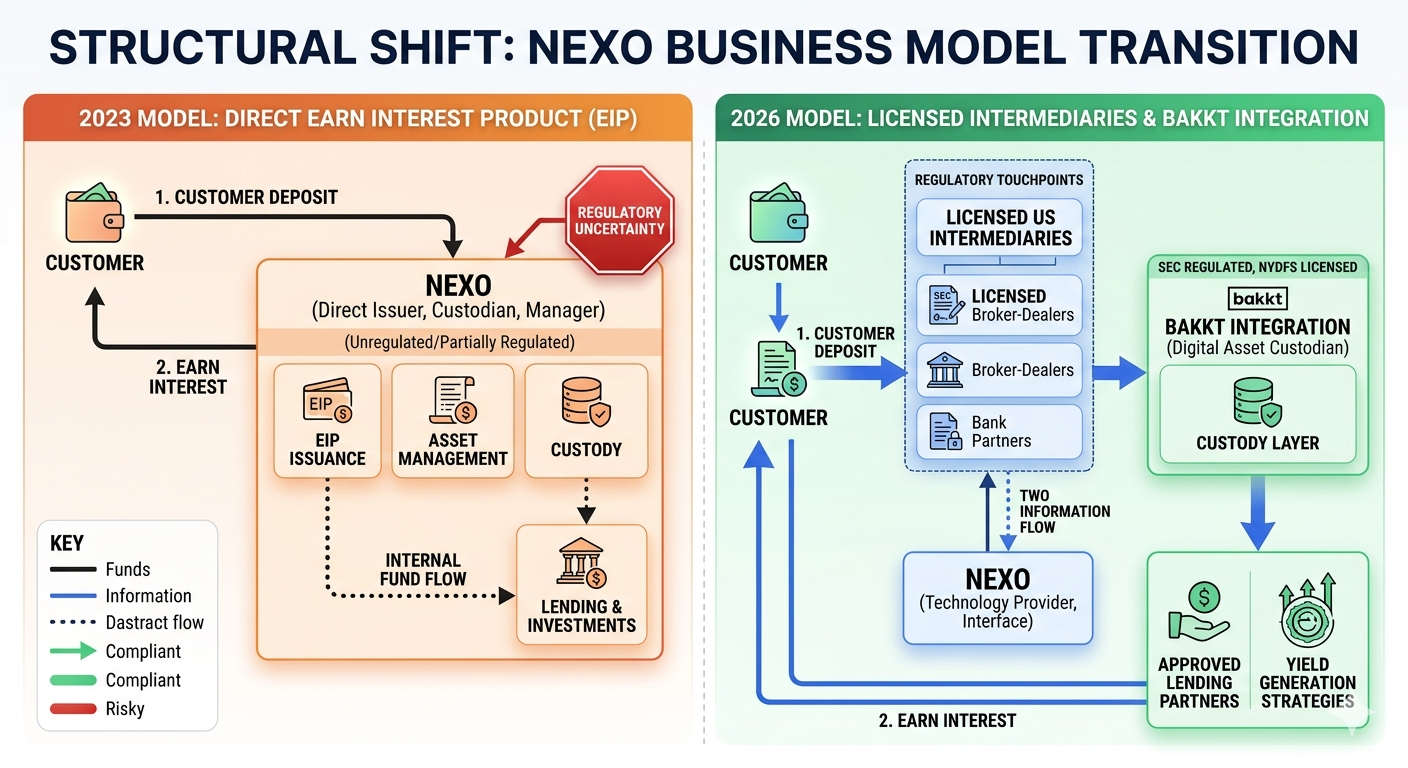

With a $45M settlement paid in 2023 and exiting the American market, Nexo has now officially re-entered the United States with a very different fundamental of a business model. As opposed to its former product offering with direct yield products, the 2026 business model is no fit for compliance, regulated intermediaries and structured association of regulated financial players.

This is no mere reentry. This is a complete architectural overhaul of how the platform functions within the US financial architecture.

Why Nexo Was Forced Out in 2023

Nexo first got attention from US investors through its Earn Interest Product a product enabling users to deposit crypto assets and earn a yield on their holdings. But by January 2023, regulatory bodies pushed back on the product‘s design and promotional messaging:

U.S. Securities & Exchange Commission said Earn Interest Product was an unregistered security. The risk was not just associated with return by itself, but the way the product was marketed and offered for sale to retail users without registration and disclosure of the product was a potential violation.

The core issues raised by regulators included:

If the retail users had been made aware of all the possible risks.

Reasons to doubt the data evidenced how the yield was produced and whether it came from pooled lending activity.

Custody arrangements and counterparty exposure

Not registered under U.S securities law (for example, not registered with the Securities and Exchange Commission or not examined by U.S auditors).

This resulted in a coordinated campaign of regulating pressure that forced Nexo to withdraw from U. S. market and settle with the settlement value of $45 million.

A Shift from Direct Yield to Regulated Intermediation

This change in Nexo which we consider the most significant, is more a matter of core structure: Nexo has transitioned from direct offering of its yield products to US users to a model utilizing regulated third parties within the US financial architecture.

Instead of being the direct counterparty for yield, Nexo transfers the services to licensed organizations such as SEC registered investment advisers when appropriate.

What this entails is of course the fact that the platform itself will be rather deemphasized, in a way that it‘s not regarded as the provider of financial returns any more. It will rather provide the technology and infrastructure to link users up to fully compliant financial institutions.

In this way, this split is intended to minimize regulatory friction and to ensure, that whichever yield related activity occurs, would be carried within the existing regulatory framework.

The Role of Licensed US Partners

One of the new pillars of the strategy is move towards the regulated partners of the US financial system. These partners will take care of custody, execution, and if needed, investment advisory.

By operating within regualted infrastructure, Nexo can circumvent directly offering securities products but still granting access to such products, through entities that are existing under US financial law.

This paradigm is indicative of broader crypto trend whereby companies are moving away from vertically integrated financial services to plug-and-play modular components for regulated entities.

Bakkt Partnership as the Compliance Anchor

At its core, Nexo‘s US reentry hinges on its partnership with Bakkt, a public traded US company which carries with it the advantage of being licensed, recognized and having relations with institutional players.

Bakkt plays the role of a compliance anchor in the new structure by offering regulated custody, trading and settlement services in the new framework. Through this partnership, Nexo now falls under an existing US framework.

Rather than issuing the yield out, Nexo essentially comes embedded in Bakkt s regulated confines pass the burden of compliance to a licensed company who is already regulated by US authorities.

From Yield Issuer to Infrastructure Layer

What (Nexo‘s) model is undergoing is a wider transition in the ways in which crypto businesses are adjusting to regulatory regimes in the US. It is transitioning from a direct financial issuer to an infrastructure provider.

In this new structure:

Alternatively, Nexo users are not dealing with Nexo at all but they are going through regulated intermdiaries.

The yield generation is managed under licensed frameworks

Custody and compliance are taken care of by US regulated entities

Nexo is centered on integration of product access and technology.

This decreases regulatory exposure without becoming ‘out of the market’.

What This Means for Users

It may seem similar for users on the surface but the workings have changed drastically. Instead of Nexo being the issuer for yield product, it will now happen through regulated partners.

This spreads the system out further but introduces added complexity. Users are introduced to multiple counterparties rather than one platform but the system is potentially easier to regulate and monitor from the regulators point of view but users will need to understand the real location of risk.

Risk Considerations in the New Model

Even though its compliant focused redesign the structure does not seem to reduce risk. It appears to just as yet again, a risk transfer mechanism to one consisting of a range of regulated intermediaries.

Key considerations include:

Too reliant on third party licensed institutions:

Differences in is option yields seem可能 to affect the transparency of production.

The regulatory burden moving with the platform onto the partners it offers its platform to.

Complexity of custody arrangements.

The model is set up to meet regulatory requirements, but investors still require an understanding of how returns are produced and where assets are held.

Evolution of Compliance: Nexo’s Structural Pivot (2023 vs. 2026)

Why This Matters for the Broader Crypto Industry

Reentry of Nexo follows a bigger pattern in crypto industry: companies are trying to fit into the established regulation rather than to struggle against it.

This transition indicates that the المقبلةrawon of cryptocurrency in the US might not be from unregulated innovation, but from combining the blockchain infrastructure and the licenced financial institutions.

It also indicates regulators aren‘t necessarily closing the door to crypto yield products as long as they are delivered through conventional, compliant means.

Conclusion

Nexo‘s homecoming signals the next wave of design in the crypto lending and yield products space. Nexo. When it returned to the US after a 2023 exit and a $45mn restitution, the company centered its design around regulation rather than product issuance.

Partnering with licensed US entities and basing its strategy off of Bakkt‘s regulated platform enabled Nexo to re-enter the market in a manner that is acceptable to regulators and accessible to US customers.

The implication is not simply a comeback story, but a templat for how crypto companies might have to do business in heavily regulated circumstances: less direct issuance, greater reliance on institutional mechanics, and an even more explicit reliance on the mainstream financial infrastructure.